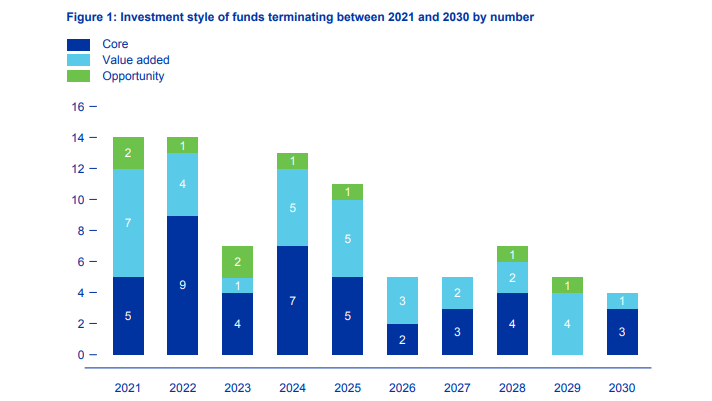

35 European closed-end, non-listed real estate funds are due to terminate between 2021 and 2023, releasing a potential €10.4 bn in Gross Asset Value (GAV) back into the market, according to the Inrev Funds Termination Study 2021 released on Wednesday.

Premium subscriber content – please log in to read more or take a free trial.