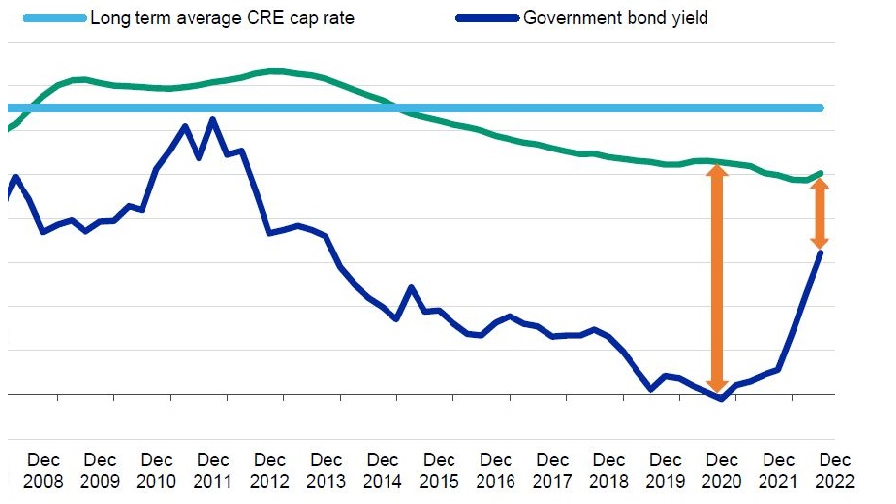

Reviewing their debt financing strategy is the highest priority for many investors, as interest rates continue to rise and values start to fall.

Premium subscriber content – please log in to read more or take a free trial.

Reviewing their debt financing strategy is the highest priority for many investors, as interest rates continue to rise and values start to fall.

The Grand Hotel Imperiale in Forte dei Marmi, Italy has been sold to UAE-based real estate company Emaar Properties, owner of renowned buildings such as the Burj Khalifa and the Dubai Mall.