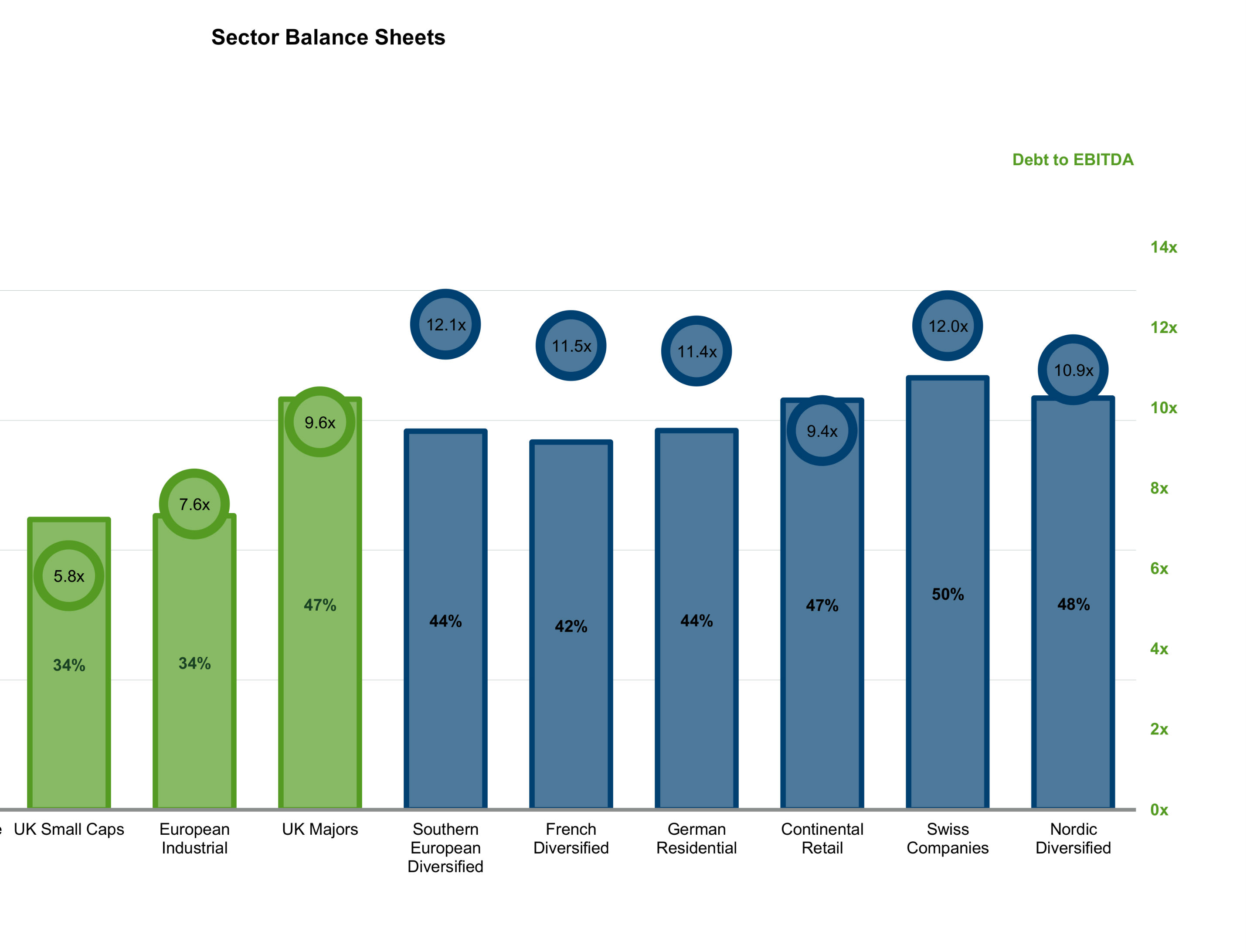

The way public property companies manage their capital structure has come under fire from real estate research firm Green Street Advisors. Debt-to-EBITDA multiples are ‘out-of-this-world high’, the firm warns in an interview with PropertyEU.

Premium subscriber content – please log in to read more or take a free trial.