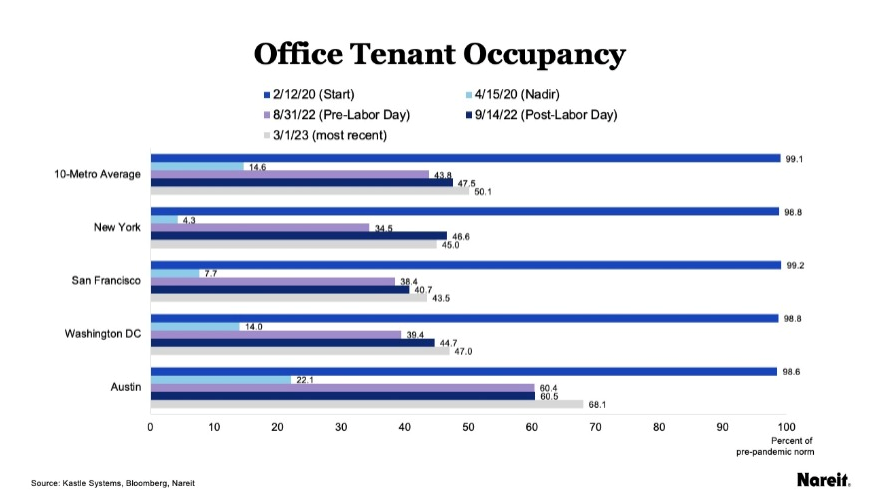

Working from the office in the US has lost its appeal for many, leading to questions over the future of the asset class. Robin Marriott reports. (long form article)

Premium subscriber content – please log in to read more or take a free trial.

Working from the office in the US has lost its appeal for many, leading to questions over the future of the asset class. Robin Marriott reports. (long form article)

Swiss real estate group Investis has boosted its real estate holdings with the CHF 139 mln (€149 mln) purchase of prime residential properties in Vaud canton.