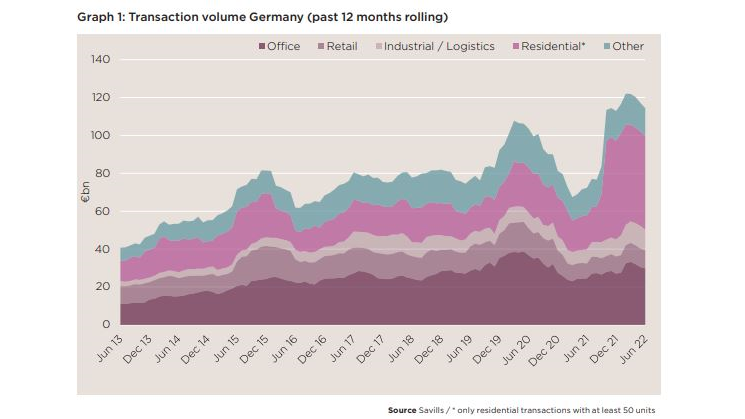

Real estate transaction volumes in Germany could end the year around 18% lower compared to 2021 levels, in a sign that the ‘exceptionally long bull market’ in Europe’s biggest market is over, says Savills.

Premium subscriber content – please log in to read more or take a free trial.