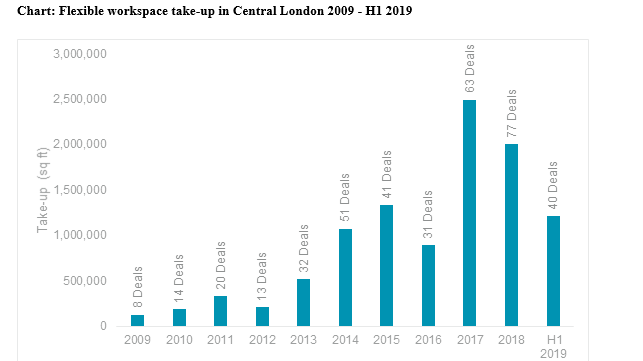

Flexible workspace is forecast to account for at least 5.5% of total office stock in Central London by the end of 2019 – three years ahead of previous forecasts, according to Cushman & Wakefield's new report, 'Coworking 2019: The UK Flexible Evolution Continues'.

Premium subscriber content – please log in to read more or take a free trial.