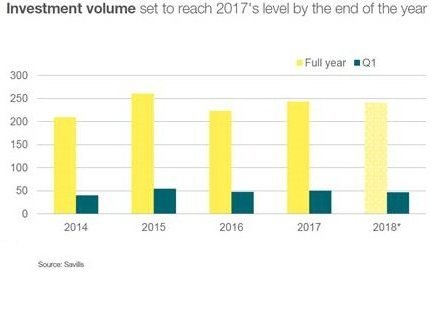

Commercial real estate investment volumes across Europe are currently on course to meet 2017 levels, after Q1 2018 was broadly in line with the long-term average, according to international real estate advisor Savills.

Premium subscriber content – please log in to read more or take a free trial.