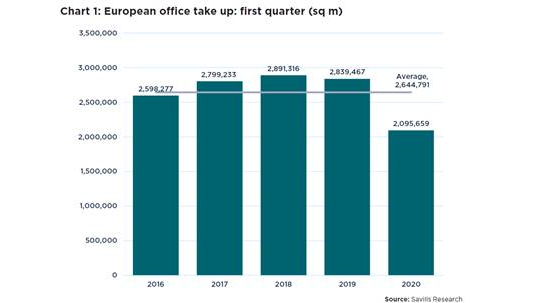

The European office market is starting to slow despite a positive start to 2020, according to Savills Spring 2020 European Office Outlook.

Premium subscriber content – please log in to read more or take a free trial.

The European office market is starting to slow despite a positive start to 2020, according to Savills Spring 2020 European Office Outlook.

International developer and asset holder Trei Real Estate has concluded 2024 with the opening of its 41st Vendo Park in Poland.