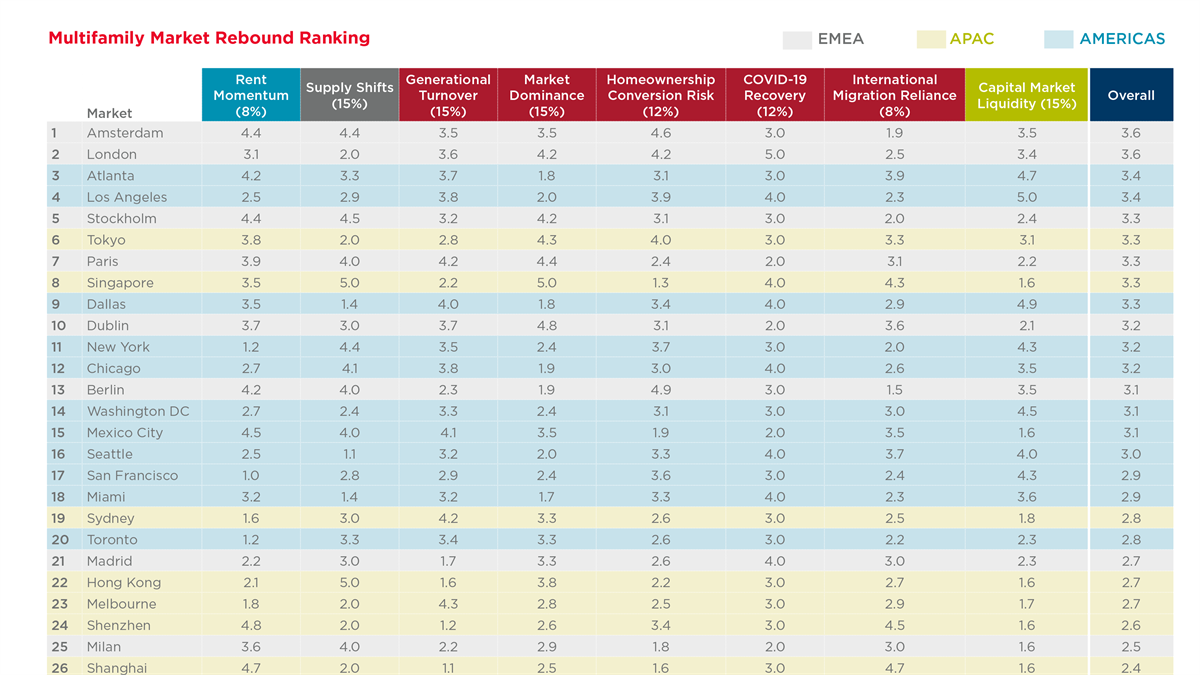

Europe’s capital cities lead the way for their rental market recovery prospects post-pandemic, with its build-to-rent markets ripe for rapid growth and investment, according to the latest research from real estate advisory firm Cushman & Wakefield.

Premium subscriber content – please log in to read more or take a free trial.