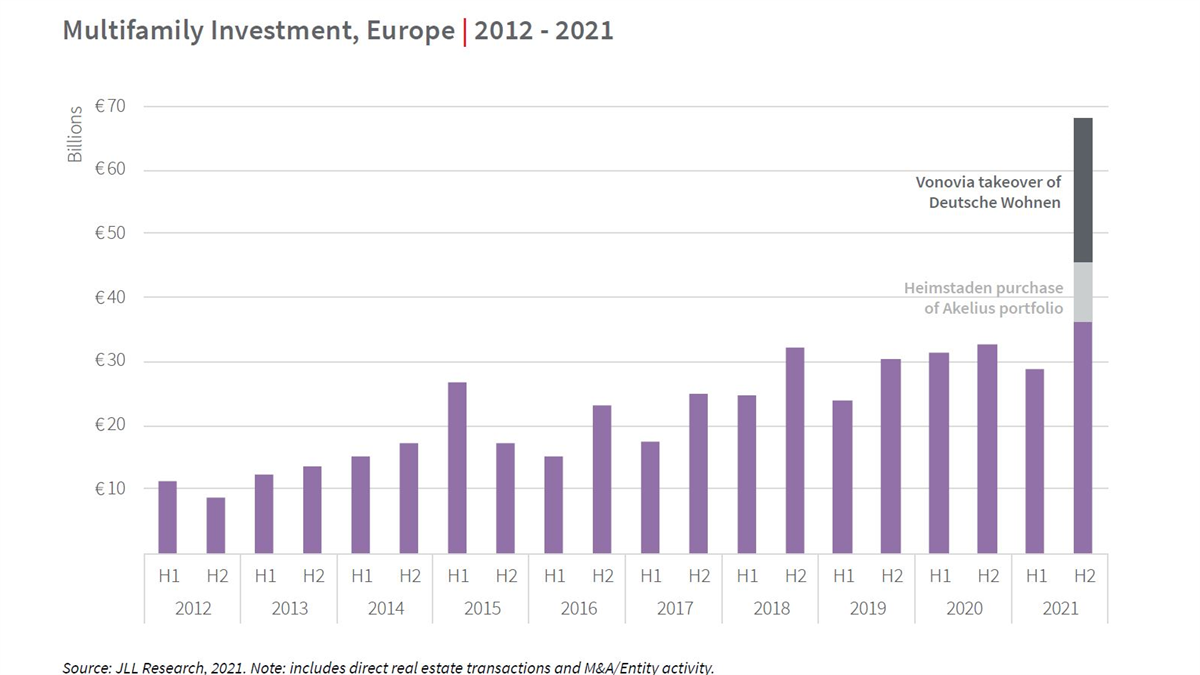

How can investors access Europe's booming but supply-strapped multifamily housing sector and where are they looking to invest? JLL's EMEA Living team share their latest insights on this red hot asset class.

Premium subscriber content – please log in to read more or take a free trial.