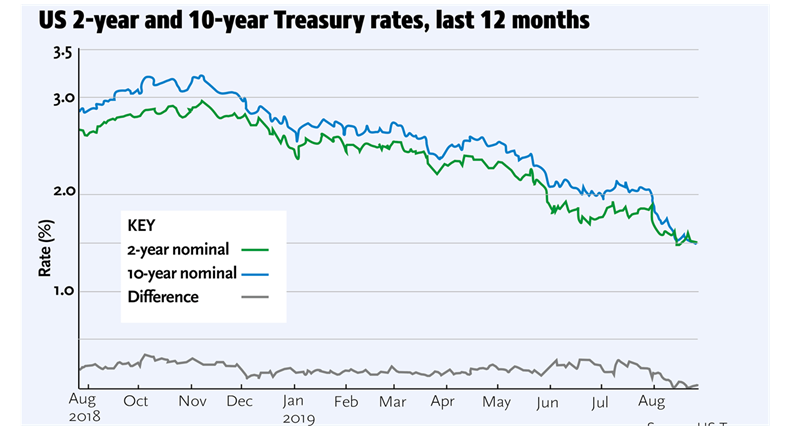

Despite jitters in the bond market, where yields on Treasury paper inverted for the first time in years in mid-August, Europe’s real estate industry remains resilient, experts say.

Premium subscriber content – please log in to read more or take a free trial.