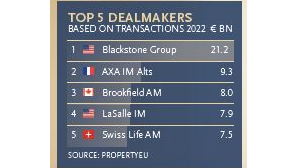

Our annual ranking of the biggest dealmakers in Europe based on transaction volume over 2022 puts Blackstone in the top spot, followed by AXA IM Alts and Brookfield Asset Management.

Premium subscriber content – please log in to read more or take a free trial.