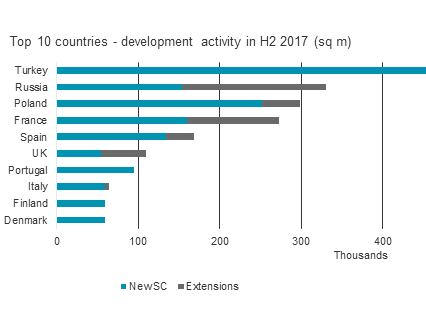

The rate of shopping centre development in Europe is slowing, with completions down 23% year-on-year at 3.8 million m2 in 2017, according to Cushman & Wakefield’s latest European Shopping Centres report.

Premium subscriber content – please log in to read more or take a free trial.