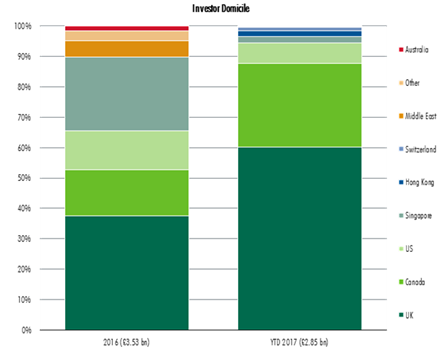

The UK student accommodation sector is continuing to attract capital from across the globe with £2.85 bn (€3.2 bn) being invested so far this year according to the latest figures from Global real estate advisor CBRE.

The report was released on the second day of Expo Real in Munich.

Over £790 mln has been invested by Canada in 2017, with Liberty Living, a student housing platform owned by Canada Pension Plan Investment Board extending its business through the purchase of the Union State portfolio for £458 mln.

Major investment has also come from Sovereign Wealth capital, with Aston Student Village, the UK’s largest single student residence being purchased for £227 mln by the LSAV joint venture between Unite and GIC, the real estate arm of the Government of Singapore Investment Corporation.

A new entrant to the market, Europa Generation, acquired six schemes from Watkin Jones known as Project Montreal with seed capital from Korean sources. Other routes to market this year have included the sector’s three REITs, with ESP having recently raised £110 mln on the London Stock Exchange to fund further acquisitions.

Portfolio deals still dominate the market by volume, and there has been a relatively small volume of solus deals with only £5.1 bn (43% of the total volume sold) in the last three years. The larger deals have shown this year that there is a strong desire for affordable product, with multiple bids for larger ensuite led opportunities and keen pricing achieved. There is still a continued demand for studios and higher rented schemes provided they are in a strong location, on a ‘boutique’ scale, and deliver on service and overall experience.

Jo Winchester, head of student accommodation at CBRE commented: 'Student accommodation is increasingly being viewed as a mainstream sector with demographically backed demand drivers and constrained supply. So far these have included not only direct let but income strips, long leases to universities or operators, bond issues and forward funding deals.

'Interestingly, the latest data from UCAS indicates that acceptances into the university system are only 1.3% less than 2016 on the same date, and higher than previous years, despite reports that overall applications into UK higher education were down by 4% for the 2017/18 compared to the same date the previous year.

'Demand remains strong from all types of investor and we expect to see further consolidation between the larger platforms driven by a strong desire to drive operational efficiencies and brand awareness through wider market coverage. Q4 will see two major student platforms, Curlew (guided at £600 mln) and Pure (£800 mln) coming to market.

'Given the continued lack of opportunities in the student sector, we expect to see the distinction with the private rented sector becoming more blurred. This could mean the increase of co-living blocks, best practice from student operating models transferring into the Build to Rent sector, or C3 residential schemes increasingly being let to students.'